| ♥ 0 |

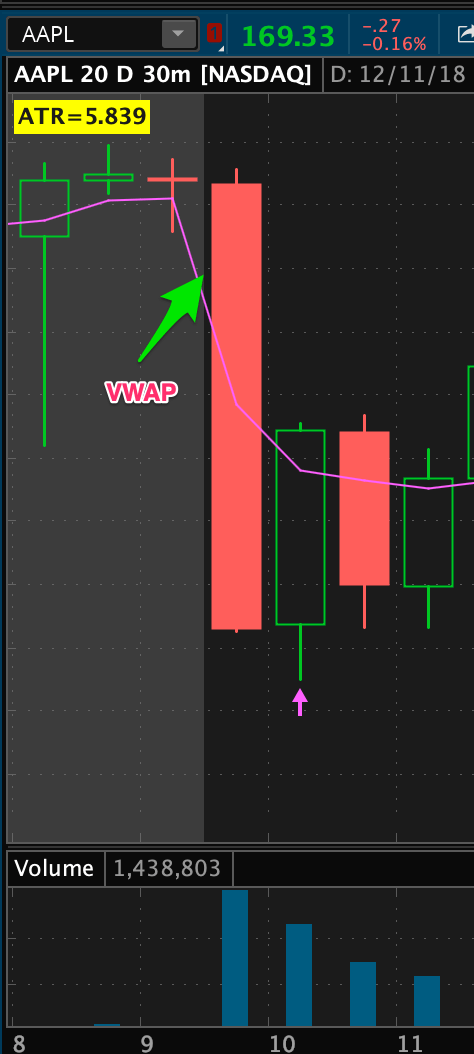

Hello I want to scan and alert when the following conditions occur. The timeframe does not matter 15 min, 30 min, etc: First candle opens above VWAP and closes below VWAP Second candle opens below VWAP and closes above VWAP Please see attached screenshot. I have not been able to figure out how to reference the 1st, 2nd, and 3rd candles of the day. Thanks in advance! Attachments:

Marked as spam

Asked on December 11, 2018 1:24 pm

318 views

|

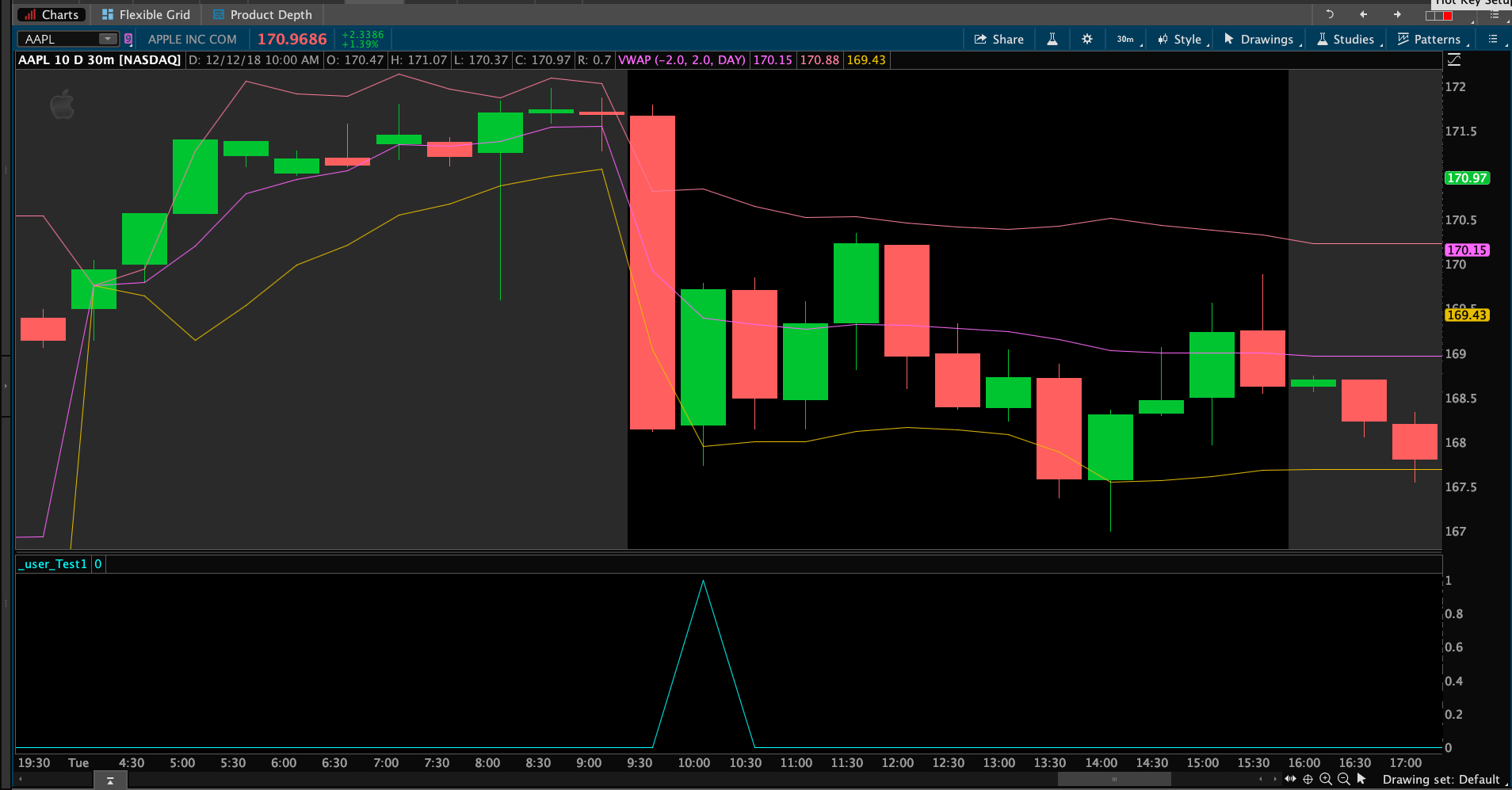

I opened the shared scan you posted in the comment above. The checkbox for extended hours was unchecked and the time frame was set to 5 min. This pattern is exceptionally rare. I believe that the lower your time frame is the more rare this signal becomes. I suggest you start with a 15 min and 30 min time frames until you start getting results.

As a test, I ran the following code on a 15 min time frame with extended hours checked. I came up with 11 results using your filters. This code looks back 39 bars to see if any valid signals occurred. It just so happens that for a 15 min time frame stocks with high after-market volume will have 40 of those 15 min candles, but only after 8 pm Eastern.

I only changed the last line in the code:

plot scan = Highest(conditionTwo, 39) > 0;