| ♥ 0 |

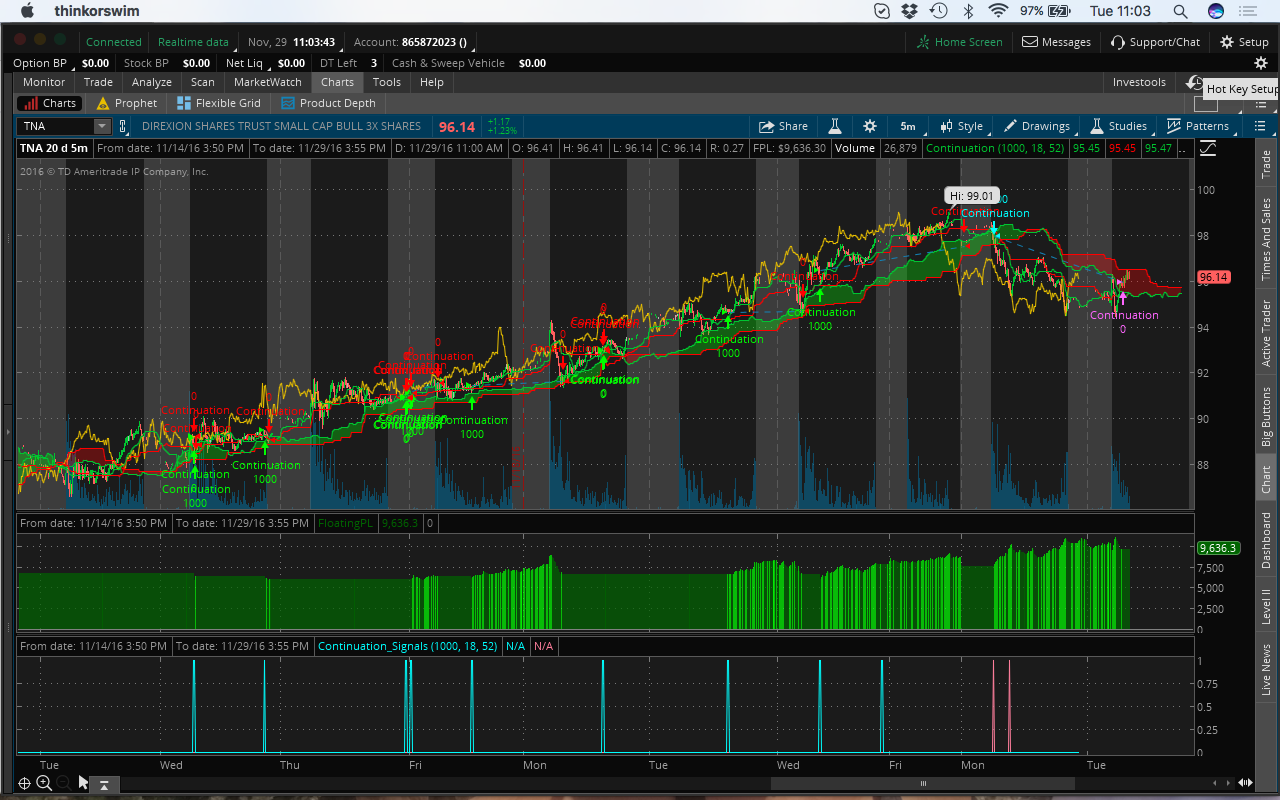

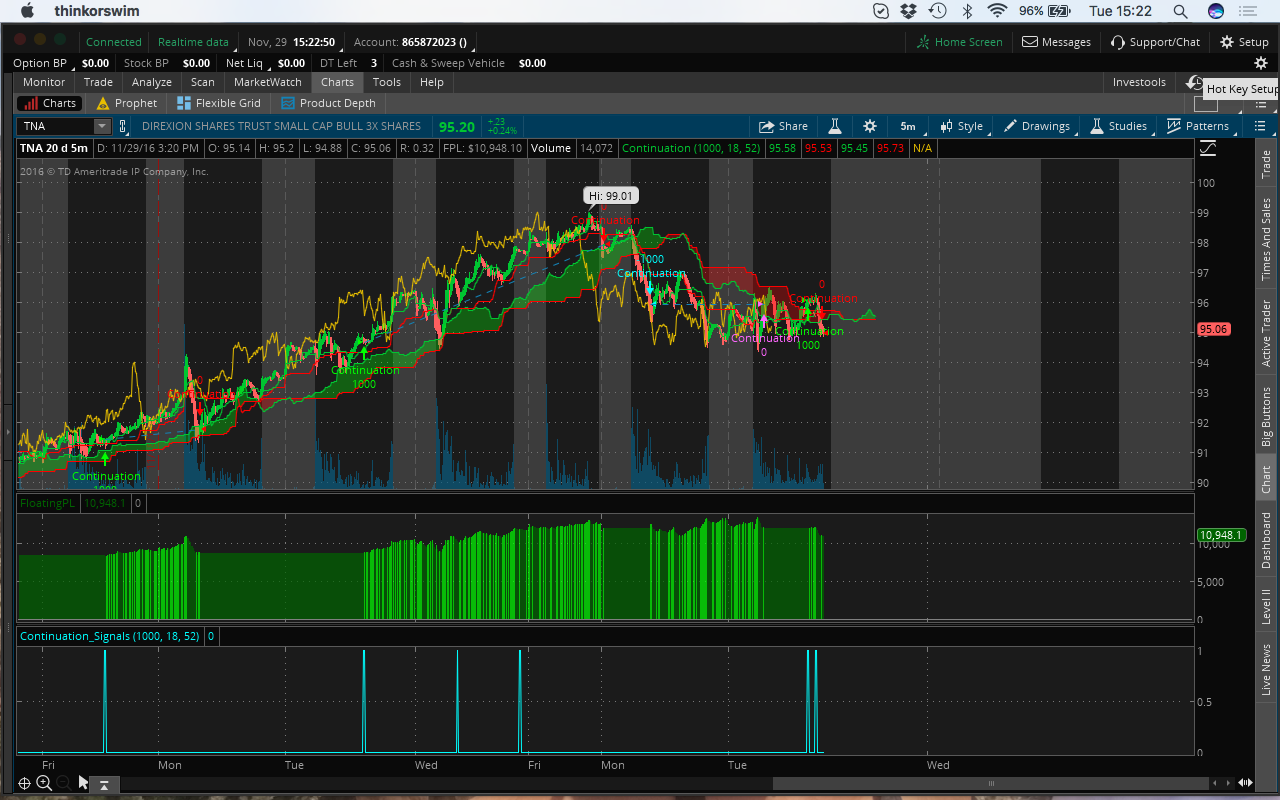

Hello! (apologies to bother again with a question but I guess other people might have run in this issue) I created a strategy based on the Ichimoku cloud system (the strategy is a continuation pattern). Then, I created a study based on the strategy (thanks again a million for your videos!). The study (see below the code) plots the entry (long and short) signals of the strategy and seems to work fine (I attach a screenshot in which you can see that the study “Continuation_Signals” seems to work fine). However, when I scan for stocks using this study as a filter the platform is unable to find a single ticker. The question is: does this happen because the study is too complicated? In case, is there a way to deal with this? Thanks again!! —– STUDY CODE —– declare lower; input tradeSize = 1000; input tenkan_period = 18; def Tenkan = (Highest(high, tenkan_period) + Lowest(low, tenkan_period)) / 2; def SpanASpanB_diff = “Span A” – “Span B”; def SpanASpanB_diff_lag = SpanASpanB_diff[-kijun_period]; def entry_long = Chikou is greater than close and Tenkan crosses above Kijun within 2 bars and SpanASpanB_diff_lag is greater than 0 and open is greater than Kijun; def entry_short = Chikou is less than close and Tenkan crosses below Kijun within 2 bars and SpanASpanB_diff_lag is less than 0 and open is less than Kijun; plot data1 = entry_long; Attachments:

Marked as spam

Asked on November 29, 2016 9:09 am

614 views

|